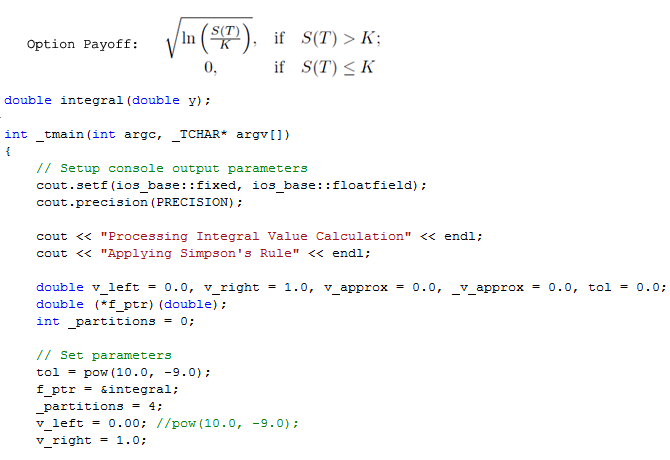

The project included development of a numerical integration model estimating values of Call Options on an underlying asset following a log-normal distribution with the observed spot, dividend and volatility parameters.

Project Type: Quantitative Finance Role: Financial Engineering | Software Engineering Technology: C++ Features: Simpson's Rule | Numerical Integration | Options Industry: Education | Financial